In this series: Minnesota 2025-26 Enrollment.

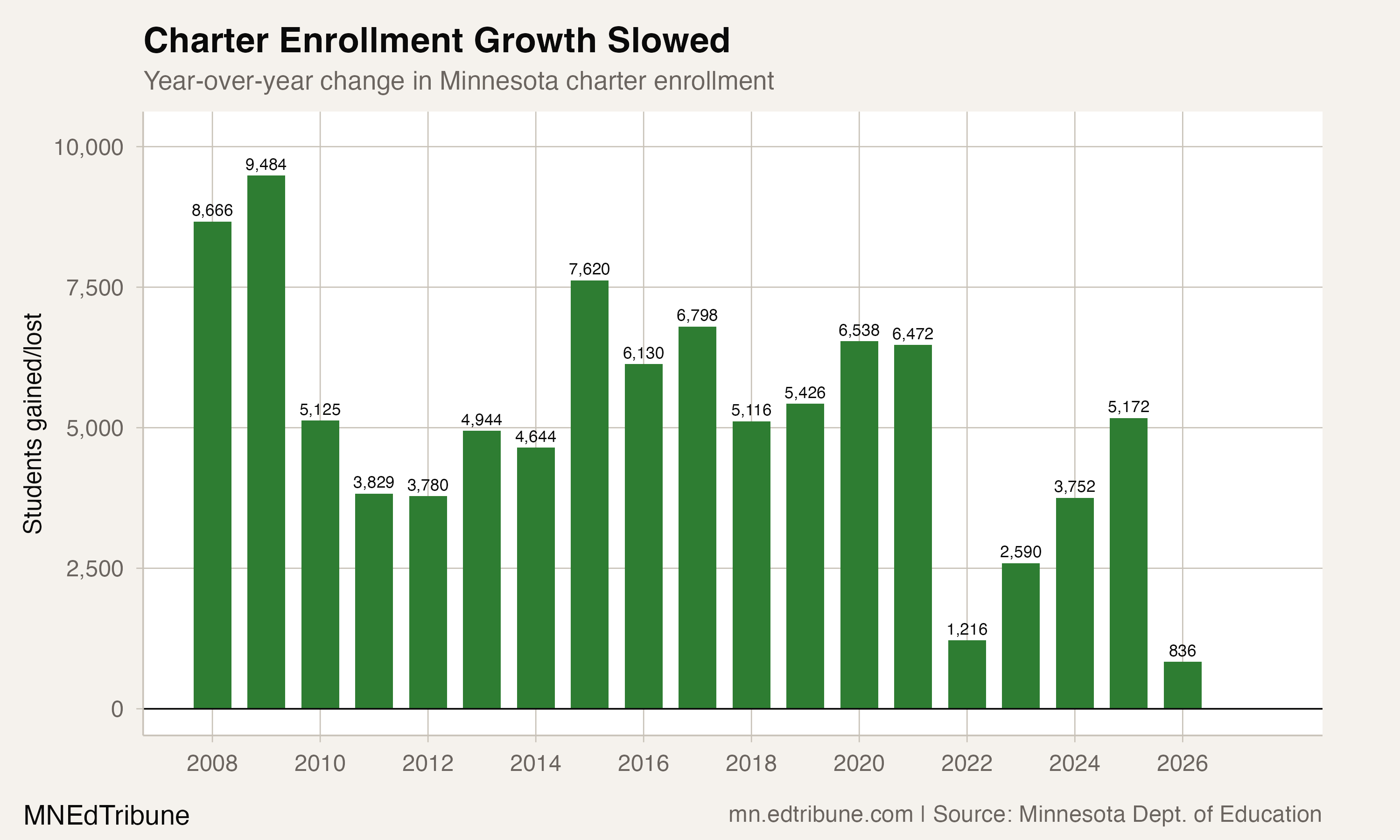

In 2008-09, Minnesota's charter sector added 4,742 students in a single year. In 2025-26, it added 418.

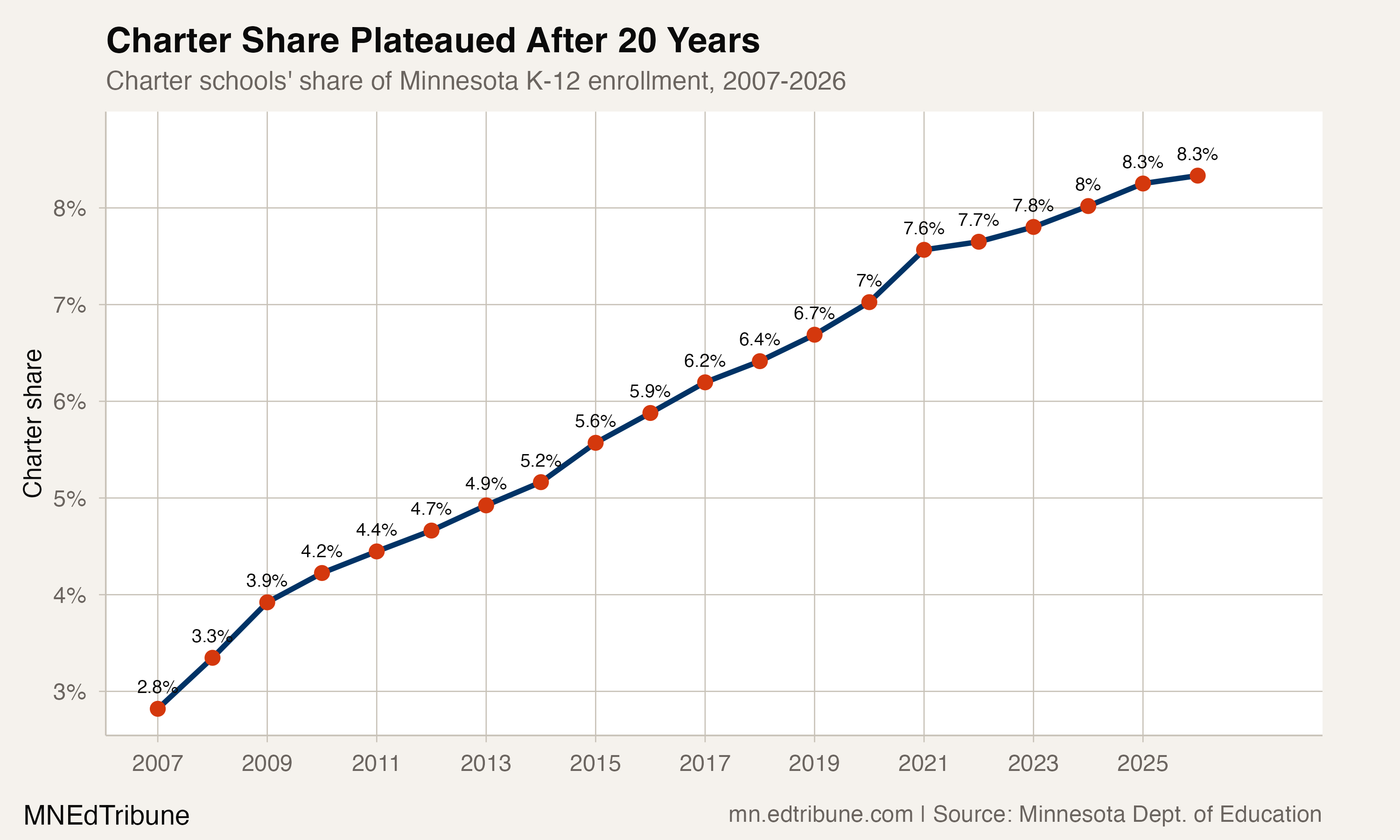

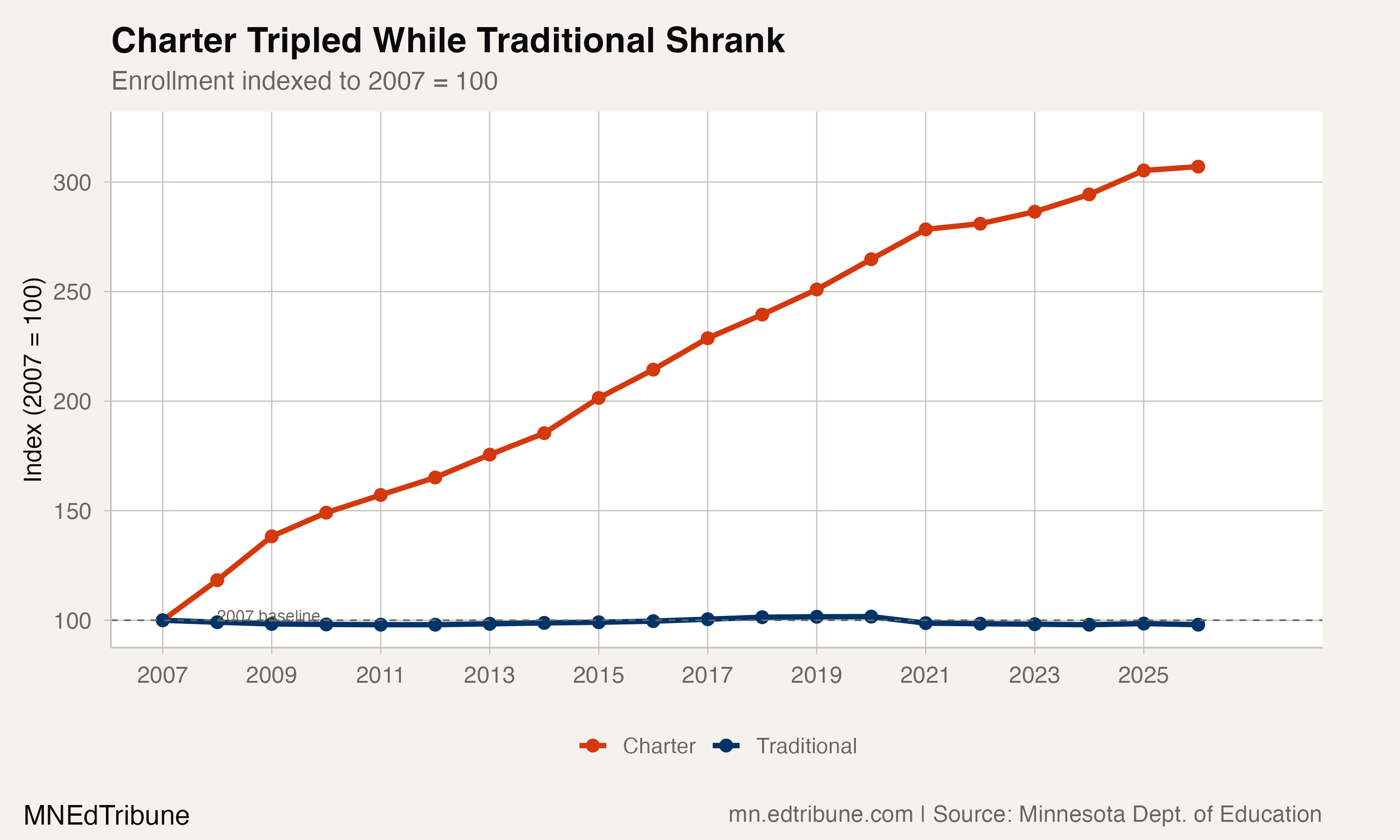

That is the smallest annual gain in the 20 years of available data, a 0.6% increase for a sector that tripled over the prior two decades. Minnesota's 169 charter schools enrolled 72,770 students in 2025-26, 8.3% of statewide K-12 enrollment, the same share as the year before. The state that passed the nation's first charter school law in 1991 has, 35 years later, hit a ceiling.

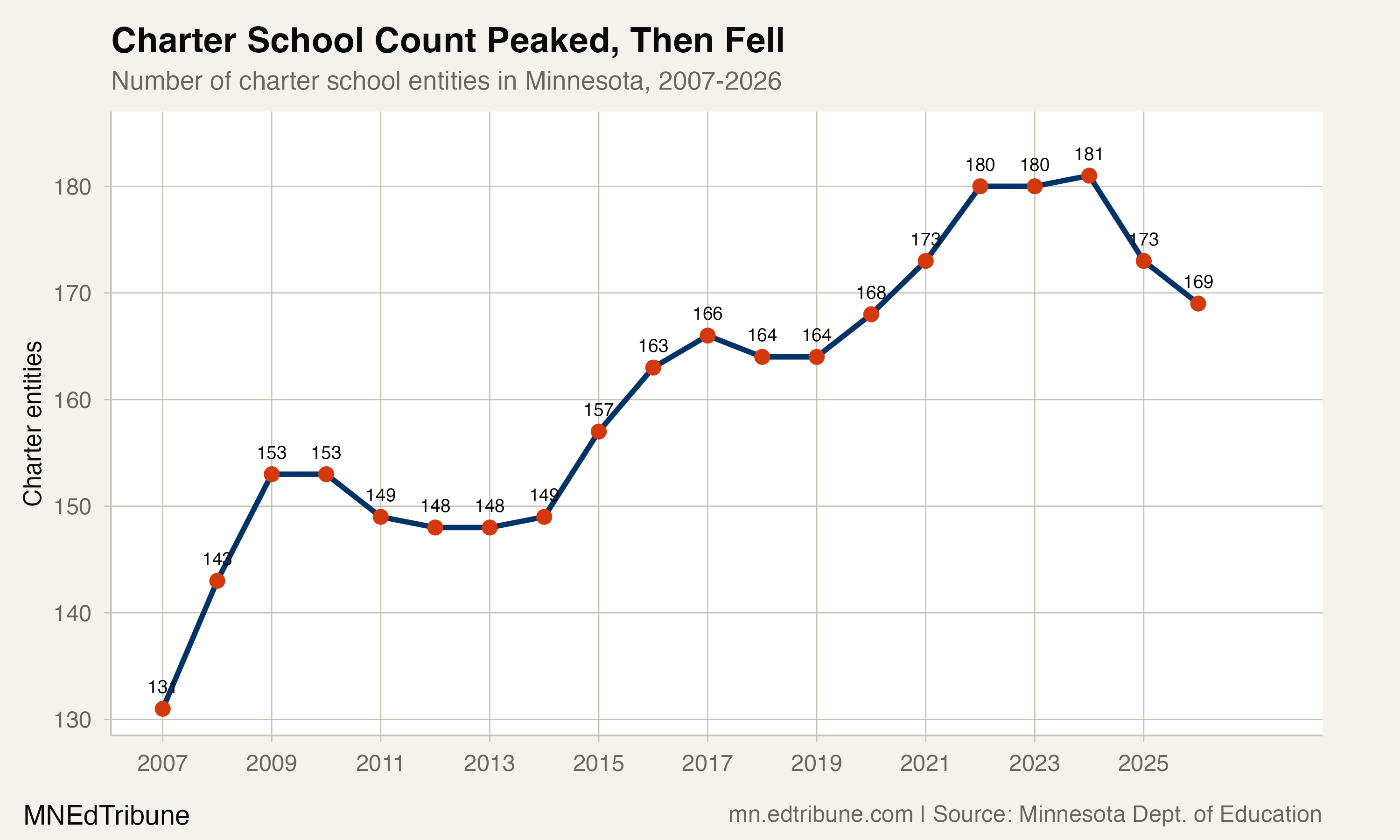

The plateau arrived just as the sector began shrinking in a different way: the number of charter entities peaked at 181 in 2023-24 and fell to 169 by 2025-26, a net loss of 12 schools in two years. Nine closed in 2024 alone, the most in a single year since the movement began.

Thirty-Five Years of Growth, Then a Stall

Minnesota's charter sector has tripled since 2006-07, from 23,701 students in 131 schools to 72,770 in 169 schools. But the growth came in three distinct eras, each slower than the last.

From 2007 to 2014, charters grew from 2.8% to 5.2% of statewide enrollment, adding roughly 2,900 students per year. New schools opened at a pace of seven to 15 annually. From 2014 to 2020, the pace slowed: share rose from 5.2% to 7.0%, with annual gains of about 3,100. Then COVID scrambled the picture. Charter enrollment surged by 3,236 students in 2020-21 as families fled traditional districts, which lost 24,356 students in a single year.

Since 2022, the picture has changed. Annual charter growth dropped to 608 in 2021-22, recovered partially to 2,586 in 2024-25, then collapsed to 418 in 2025-26. Share gains decelerated from half a percentage point per year during COVID to 0.08 points in 2025-26.

The 418-student gain in 2025-26 is worth comparing to the traditional sector's loss of 3,989 students that same year. Charters are no longer growing fast enough to absorb even a fraction of the students leaving traditional districts. The traditional sector actually gained 4,193 students in 2024-25 before giving them right back.

The Closure Wave

Of the 245 charter entities that have appeared in state enrollment data since 2006-07, 76 have closed. That is 31%, closely matching a Sahan Journal investigation that found one-third of all Minnesota charters ever opened have shuttered.

The closures accelerated sharply in 2023-24 and 2024-25. Nine entities disappeared from state data in 2024, including LoveWorks Academy for Arts, which at its peak enrolled 362 students, and Upper Mississippi Academy in St. Paul, which had 313 students before financial difficulties forced its doors shut. Five more closed in 2025, including Athlos Academy of Saint Cloud, which had reached 687 students before its authorizer declined to renew its contract.

New openings have nearly stopped. Only one new charter entity appeared in state data in each of the last three years, down from 10 in 2021-22. The net effect: 14 fewer charter schools operating in Minnesota than two years ago.

Who Charters Serve

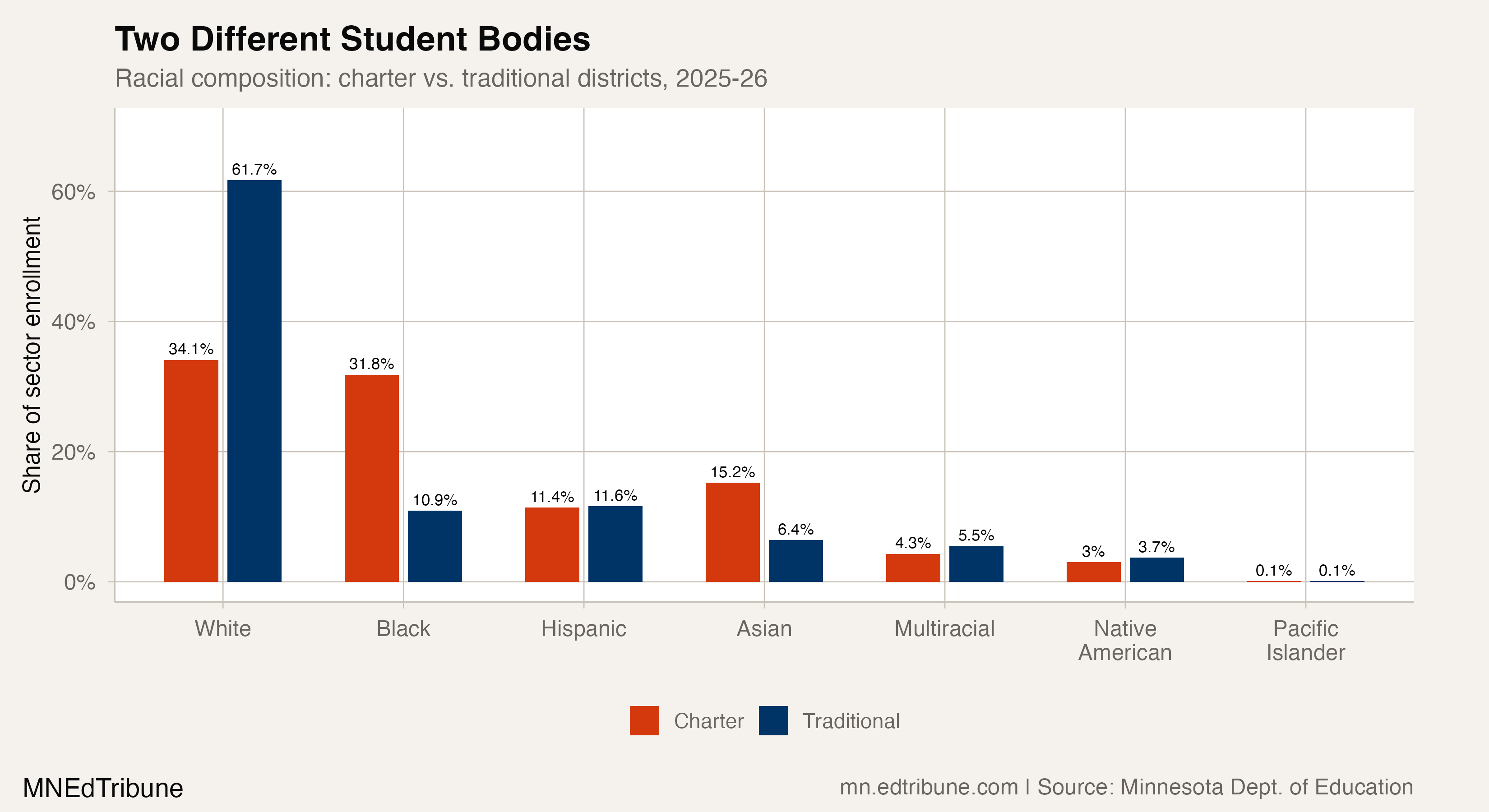

The sector's demographics explain both its political importance and the stakes of its stagnation. Minnesota's charter schools serve a fundamentally different student body than its traditional districts.

Black students make up 31.8% of charter enrollment but 10.9% of traditional enrollment, a ratio of 2.9 to 1. Asian students, many from Minnesota's large Hmong community, comprise 15.2% of charter enrollment versus 6.4% in traditional districts. White students are 34.1% of charter enrollment, compared with 61.7% of traditional districts.

Hmong College Prep Academy↗ET in Brooklyn Park enrolls 2,456 students and serves a predominantly Hmong student body. Higher Ground Academy↗ET in St. Paul, which enrolls 1,177 students, serves a nearly 100% Black, predominantly Somali community. Hiawatha Academies↗ET in Minneapolis grew from 145 students in 2008 to 1,683 in 2026. These are not schools that exist to offer suburban families an alternative to their already-functional district. They are institutions built around specific communities.

That makes the charter ceiling a different kind of problem than it would be in states where charters primarily serve as escape valves from large urban districts. In Minnesota, a shrinking charter sector means fewer options for communities that built schools specifically because the traditional system was not serving them.

What Stopped the Growth

The most direct factor is arithmetic. New openings dropped to one per year while closures surged to nine. No sector can grow when it is losing more schools than it creates.

But the reasons behind the closure wave are themselves contested. Charter advocates point to a hostile funding environment: Minnesota charters receive roughly 70% of the per-pupil funding that traditional districts get, since they receive state funds but not local property tax revenue. Governor Walz's 2025-26 budget proposal would cut an additional $40 million from charter funding, including eliminating long-term facilities maintenance support and special education tuition adjustments.

"Charter schools are currently asked to operate with 30 percent less funding than their public-school counterparts." — Letter to Minnesota Legislature, cited in City Journal, 2025

On the other side, the Minnesota Department of Education has increased accountability requirements, creating three dedicated fraud detection positions and requiring authorizers to file more than 1,000 pages of documentation per school annually. The 2024 legislative session imposed new charter requirements, including language access plans, procurement policies, and documentation mandates that add administrative burden to an already-stretched sector. Proponents of stronger oversight argue that closures represent the system working as intended: low-performing schools exit, protecting students from sustained failure.

The national picture suggests Minnesota is not alone. The Network for Public Education reported that 50 charter schools nationwide announced closures in the first half of 2025 alone, adding to 218 that closed or never opened between 2022 and 2024.

Consolidation, Not Collapse

The data tells a story that is more nuanced than either "charters are dying" or "charters are thriving." What is actually happening is consolidation. The average charter school in Minnesota enrolled 431 students in 2025-26, up from 181 in 2006-07. Small, fragile charters are closing. Larger, established ones are stable or still growing.

Minnesota Transitions Charter School↗ET, the state's largest charter, grew from 1,274 students in 2007 to 6,425 in 2026, with a COVID-era surge from 3,593 to 5,508 in a single year. Metro Schools Charter quadrupled from 400 students in 2020 to 1,643 in 2026. But the schools that closed were almost all small: of the 23 charters that closed since 2020, the median peak enrollment was 105 students. Only four ever exceeded 350, and only one, Athlos Academy of Saint Cloud at 687, could be considered mid-sized.

This consolidation pattern carries a risk. The charter sector is increasingly dependent on a small number of large operators. If a school like Minnesota Transitions, which alone accounts for 4.4% of all charter enrollment, were to face difficulties, the impact would ripple across the sector's enrollment totals.

The Question Minnesota Invented

Minnesota passed the nation's first charter school law on June 4, 1991. The original statute allowed a maximum of eight schools, with only school districts authorized to sponsor them. That cap was lifted, the authorizer framework was expanded, and by the mid-2000s the sector was growing at double-digit rates.

Thirty-five years later, the state's charter share sits at 8.3%, and the growth engine has stalled. Whether that represents a natural market equilibrium, the accumulated effect of a funding structure that starves smaller schools, or something else entirely depends on which side of the charter debate you occupy. The data cannot adjudicate between those explanations.

What the data does show is the next pressure point. The pressure is no longer just Governor Walz's proposed $685 million in education cuts over four years: the enacted 2025 K-12 budget included reductions such as lower special-education transportation reimbursement and a $250 million special-education savings target for the next biennium. The nine closures in 2024 happened before those cuts take effect. The 2026-27 enrollment numbers will reveal whether the plateau becomes a decline.

Detailed code that reproduces the analysis and figures in this article is available exclusively to EdTribune subscribers.

Discussion

Sign in to join the discussion.

Loading comments...